Penn’s endowment has felt the impact of a financial crisis thousands of miles away.

On Friday, the University announced a 1.6-percent endowment return for fiscal year 2012, which ended on June 30.

Penn’s modest return follows two stronger years of investment performance. The University’s endowment — which is managed primarily through the Associated Investments Fund — saw returns of 18.6 and 12.6 percent for FY 2011 and FY 2010, respectively.

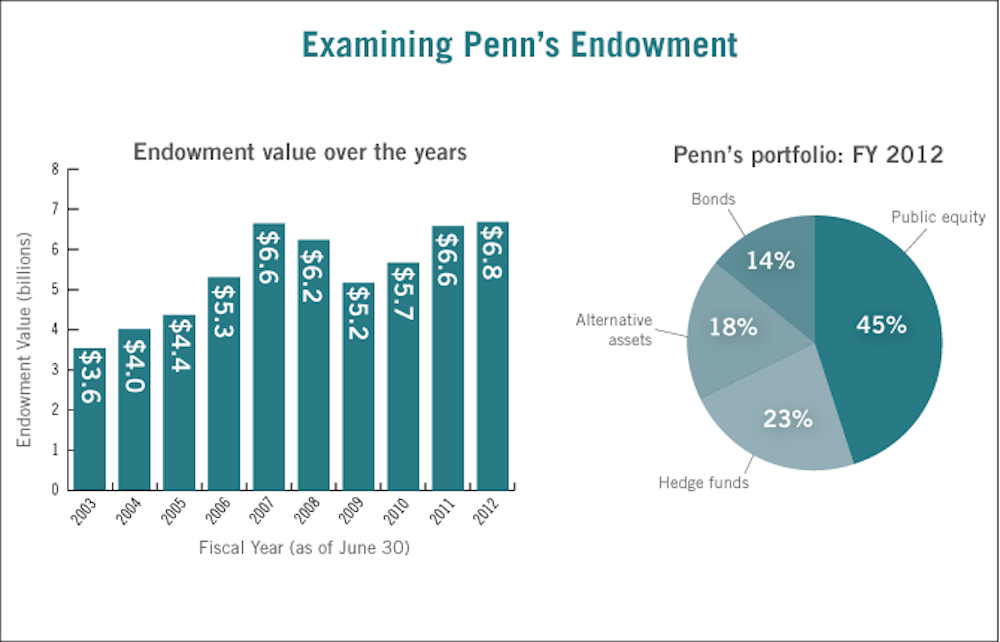

The $172 million net increase in endowment funds — which accounts for investment gains, gifts, spending and net transfers — brought the total endowment to $6.8 billion at the close of FY 2012. The endowment stood at $6.6 billion at the close of FY 2007, before it shrank as a result of the recession.

Chief Investment Officer Kristin Gilbertson cited the eurozone debt crisis as a “challenge” to Penn’s investment performance.

“The return is not inspiring, but it should not be unexpected, given what happened in global equity markets for the fiscal year,” she said. “In the context of what happened in the global equity market, a 1.6-percent return is actually pretty good.”

Penn’s results contrast with a 5.5-percent gain — which includes reinvested interest — reported by the Standard & Poor’s 500 Index.

Though peer institutions have not yet announced endowment performance, an Aug. 6 report by consulting firm Wilshire Associates said that endowments and foundations experienced a median return of just 0.37 percent in FY 2012. This marked the lowest average return of any class of institutional investor, according to the report.

Penn’s portfolio for FY 2012 was composed of 45 percent public equity, 23 percent hedge funds, 18 percent alternative assets and 14 percent bonds, Gilbertson said. The top performers in the portfolio were illiquid assets — which describe generally riskier investments that are not easily converted into cash — including real estate, natural resources and public equity.

Over the years, Penn has moved to diversify its portfolio to include more risk: the percentage of illiquid assets in the portfolio has tripled since Gilbertson became CIO in 2004.

John Griswold, executive director of the Commonfund Institute — which researches endowments and investment practices — was not surprised with Penn’s marginal return, given the current economic climate.

“I think this will be a tougher year coming out because there is a great deal of uncertainty about a number of economic situations,” he said. “It won’t be surprising to see single-digit returns on average.”

Executive Vice President Craig Carnaroli agreed that the numbers were more of a reflection of the market conditions than of the performance of the University’s asset managers.

“The returns are consistent with the general volatility, the challenges seen worldwide and the sluggish economy as we come out of this recession, so I think it’s consistent with that,” he said.

Wharton finance professor Christopher Geczy said the University could have avoided short-term consequences of the eurozone crisis by “tilting away from Europe,” but that this move could have held more long-term risk.

“I think they always have to be concerned about the long term because we have a long horizon for the endowment,” he said. “That’s a very important perspective to have because it pushes us to diversify our portfolio.”

The longer-term annualized returns for Penn’s endowment paint a more positive picture for the University’s investments moving forward. The three- and ten-year annualized returns at the close of FY 2012 were 10.7 and 7 percent, respectively.

Carnaroli said the general growth of the endowment has enabled Penn to increase the distribution set by its spending rule — a formula that calculates how much of the endowment can be used in the annual budget. For FY 2012, 8 percent of the operating budget was supported by the endowment, while only 6 percent came from the endowment in 2002.

However, the average Ivy League endowment covers roughly 20 percent of each school’s operating budget annually, Carnaroli told The Daily Pennsylvanian last year.

Carnaroli said the slower growth in the endowment will not have immediate effects on Penn’s operations, but “it will slow the rate of growth in our five-year parameters for the spendable endowment income that comes into the budget.”

Looking to the future, the single-digit return will not scare the investment team away from the public equity market, Gilbertson added.

“Though this has been a tough year, we think that valuations are attractive … and we are guardedly optimistic about the outlook for the next three to five years,” she said. “We’re getting paid to take the risk that we do of running a fully invested portfolio.”

Carnaroli agreed.

“I don’t see any need for concern over a one-year number,” he said. “Penn has existed for 270 years … and we manage our investments for the long term.”